Editor’s note: This is part of the Affordable Housing Series.

Affordable housing borrowers in Vermont aren’t being expected to pay back loans, but that arrangement raises questions about IRS definitions of a bona fide loan in low-income tax credit projects.

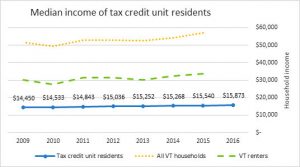

Despite the common perception that affordable housing occupants can’t be expected to help repay affordable housing loans, evidence suggests that their incomes actually tend to rise over time.

In one of the few studies on the subject, a Gov. Jim Douglas-era report on affordable housing showed incomes of Vermonters in low-income housing were in a slight upward trend. The report’s data demonstrated that many low-income loans should be repaid to better help the state’s bottom line.

What is the trend since 2009, when that report published?

Data supplied by the Vermont Housing Finance Agency shows the trend continues upward.

“Since 2009, median household income among Vermont’s tax credit unit residents has changed very little, increasing 1.4 percent each year on average — less than the 2 percent rate among all renters in the state, as of 2015,” VHFA Director Susan Carpenter told True North in a July 24 email.

Among all Vermont households (both owners and renters), median household income increased by 1.7 percent annually on average between 2009 and 2015. (VHFA graph)

In a June interview with True North Reports, Carpenter said Vermont’s affordable housing program doesn’t want to raise rents to help pay back loans because “if the incomes of the residents remain low … there is no room in the rents to pay back these loans.”

But if the state doesn’t expect borrowers to repay, that raises questions about whether or not the loans meet the IRS definition of a bona fide loan in low-income tax credit projects.

As defined by IRS guidelines, a bona fide debt is one “which arises from a debtor-creditor relationship based upon a valid and enforceable obligation to pay a fixed or determinable sum of money.”

“An essential element of bona fide debt is whether there exists a good-faith intent on the part of the recipient of the funds to make repayment and a good-faith intent on the part of the person advancing the funds to enforce repayment,” according to IRS statute on the Low-Income Housing Credit.

As enacted by Congress as part of the Tax Reform Act of 1986, the purpose of the credit was to encourage new construction and rehabilitation of existing buildings as low-income rental housing for households with income at or below specified income levels.

Do Vermont’s affordable housing loans meet IRS guidelines? It’s hard to find out. According to the website of the U.S. Government Accountability Office (GAO), “the Internal Revenue Service oversight of the Low-Income Housing Tax Credit program has been minimal.”

GAO reports that since 1986, the IRS conducted only seven audits of 56 state housing finance agencies (HFAs) on which the federal tax agency relies to administer and oversee the program.

Thus, it appears unlikely that a state entity in violation of federal law would come under IRS scrutiny.

“Without such reviews, IRS cannot determine the extent of noncompliance and other issues at HFAs,” GAO states.

Lou Varricchio is a freelance reporter for True North Reports. Send him news tips at lvinvt@gmx.com.

A “loan” made with no expectation of repayment is nothing more than a gift. PERIOD.

That said loans are made at the expense off taxpayers is fraudulent.

Lending money to folks knowing full well that the money will never be paid back is the very thinking which caused the housing bubble to burst several years ago. I recall when the Congress wanted to require a 20% down payment to buy a house there was all kinds of push back because there was concern that no one in the lower income brackets could afford to buy a home. The 20% requirement never flew and a mess was created. Why not be honest with the tax payers and tell us that X% of our tax dollars will be a donation to the Low Income Housing 501 3(c) charity so we can take a charitable donation deduction on our income tax return?